Scope semi-annual Review

60% of transactions set to underperform in 2022

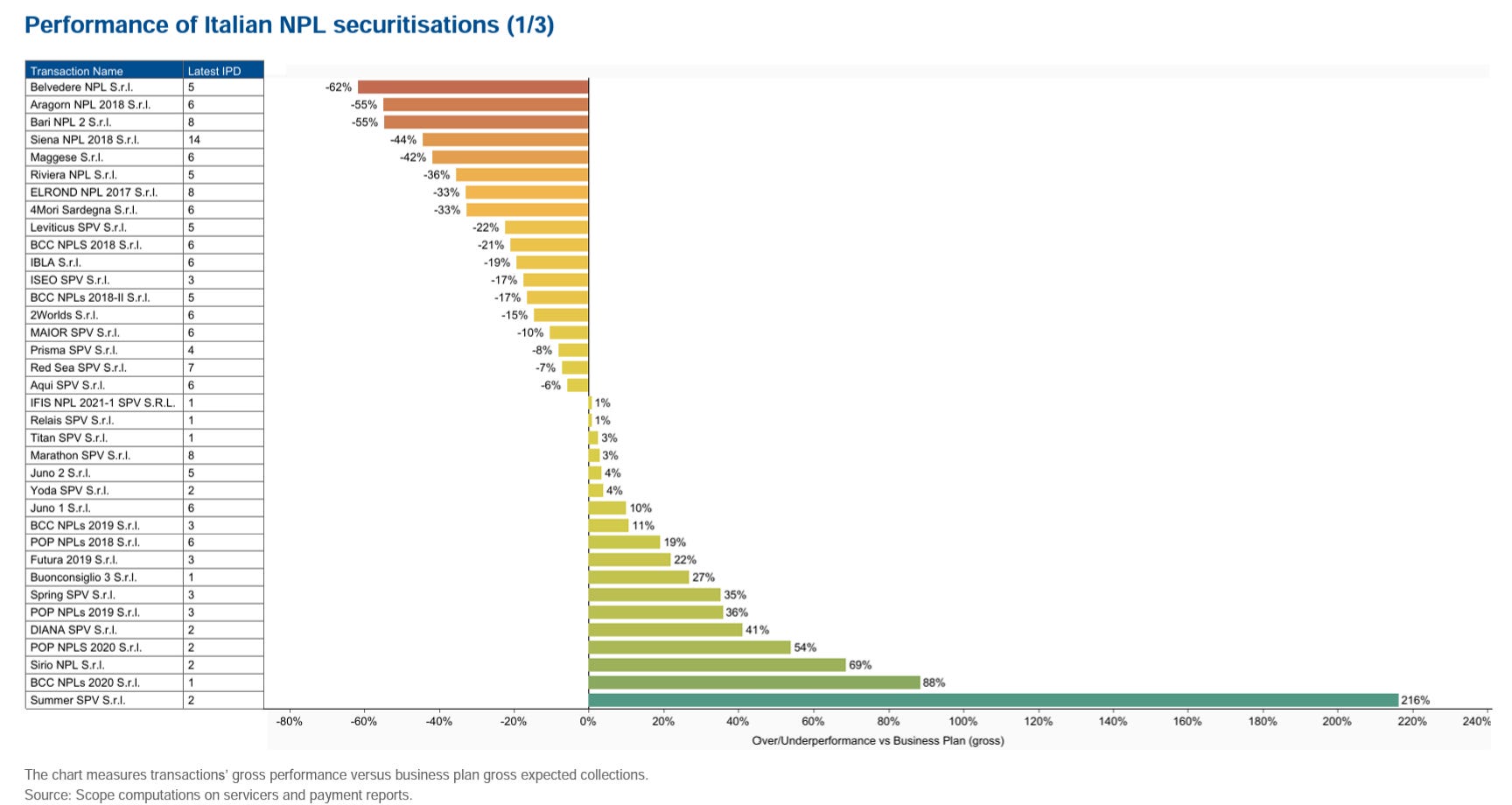

Scope Ratings published its Semi-annual Italian NPL review and outlook stating that the performance of Italian NPL securitisations in the second half of 2021 failed to show any major improvements from first-half figures. Collection volumes on half of the transactions were 30% below business plan expectations while the other half over-performed by an average of 35%.

This evidences high performance volatility. The median profitability on closed positions was at 87% of Scope´s B case assumptions. In the short term, sector performance will remain weak and uncertain as the economic consequences of the pandemic and disruptions to the legal system work themselves through the system. In the medium to longer term, however, we expect an improvement. But even then, transactions with weak underlying portfolio quality and those that had overly optimistic business plans at closing will continue to underperform against business plans. Scope tracks performance both against business plan expectations and our own projections.

Relative to business plans, we generally focus on the timing of collections, and complement the analysis on profitability by referencing our own projections at closing. We have downgraded the senior notes of 17 out of 36 transactions by an average downgrade of two notches. Our proprietary NPL indices reflect weakness in the underlying market. The NPL Performance Index (NPI), which tracks cumulative collections against servicers’ original projections, stands at 85. The Index reflects material under-performance of NPL transactions against their original business plans (i.e. below the baseline of 100). Scope expectation is that notes will amortise in six to eight years, based on our NPL Dynamic Coverage Ratio Index (SCI), which tracks the speed of note amortisation.

By the end of 2022, Scope estimates that 60% of the transactions analysed in its report will show collection volumes lagging servicers’ forecasts by an average of 30%, while the remainder will over-perform by an average of 50%. Profitability on closed positions is expected to remain about 90% of Scope’s B case scenario.

The European Banking Authority (EBA) published today a Report which analyses the recent developments and challenges of introducing sustainability in the EU securitisation market. The EU sustainable market is still at an early stage of development and the application of sustainability requirements in securitisation appears to require further clarification. The Report examines how sustainability could be introduced in the specific context of securitisation to foster transparency and credibility in the EU sustainable securitisation market and to support its sound development.

In particular, the Report explores the following aspects:

whether and how the EU regulations on sustainable finance, including the EU Green Bond Standard (EU GBS), the EU Taxonomy, and the Sustainable Finance Disclosure Regulations could be applied to securitisation;

the relevance of a dedicated regulatory framework for sustainable securitisation and;

the nature and content of sustainability-related disclosures for securitisation products.

The EBA’s analysis shows that it would be premature to establish a dedicated framework for green securitisation. Rather, the EBA is of the view that the upcoming EU GBS regulation should also apply to securitisation, provided that some adjustments are made to the standard. In this regard, the EBA recommends that the EU GBS requirements apply at originator level (instead of at the issuer/ securitisation special purpose entity (SSPE) level). This would allow a securitisation that is not backed by a portfolio of green assets to meet the EU GBS requirements, provided that the originator commits to using all the proceeds from the green bond to generate new green assets.

The EBA sees the proposed adjustments as an intermediate step to allow the sustainable securitisation market to develop and to play a role in financing the transition towards a greener EU economy. They are also meant to ensure that securitisation is treated in a consistent manner as other types of asset-backed securities.

The EBA also recommends that the Securitisation Regulation is amended in order to extend voluntary ‘principal adverse impact disclosures’ to non-STS (simple, transparent and standardised) securitisations. It also calls for further EBA work on green synthetic securitisation and social securitisation.