New Publication by EY on credit and NPE Market

NPE Market Update del 11 ottobre 2021

EY launched a new quarterly publication that aims to monitor key developments in European credit and NPE markets during the current downturn and beyond. After a long period in hibernation, the full credit implications of the COVID-19 pandemic are starting to emerge into daylight.

More specifically, the Q1-21 NPE tracker shows that:

SMEs were among the leading users of European bank credit during Q1-21

European asset quality remains finely balanced, although there are signs of coming deterioration

Moratoria and public guarantees have laid the ground for a consumer-led recovery, but could harbor pockets of risk

NPLs look set to increase — but to a manageable level

In short, it seems likely that, as payment moratoria and public guarantees come to an end, the second half of 2021 will see the European credit downturn move out of its current holding pattern. By the end of the year, we should have a much clearer idea of the areas where provisioning and losses are growing — and of which sectors are likely to see the greatest transaction activity.

Luigi Luzzatti S.C.p.A. e il Gruppo Prelios hanno siglato un Memorandum of Understanding per la costituzione di un nuovo fondo di investimento alternativo chiuso riservato ai crediti distressed classificati come Unlikely to Pay. Il fondo, i cui principali contributori saranno le banche azioniste di Luzzatti, investirà in crediti UTP vantati da aziende in gran parte del segmento PMI/Corporate. Metterà in atto strategie di recupero crediti volte a rimettere in bonis le aziende debitrici, attraverso una gestione proattiva delle loro posizioni focalizzata sulla ristrutturazione aziendale.. Leggi l’articolo.

Mediobanca Credit Solutions, ha reso nota la sottoscrizione di un accordo con Intesa Sanpaolo per l’acquisto di un portafoglio di crediti unsecured originati sia verso una clientela di tipo retail , sia verso clienti SME che corporate per un totale di circa 2,6 miliardi e oltre 42mila controparti. Leggi l’articolo.

#Savethedate 18 ottobre 2021 8° Concgresso di Giurimetria Banca e Finanza organizzato da Almaiura. Link all’evento.

Onorato di partecipare come relatore alla tavola rotonda "NPL e Fondi Alternativi d'Investimento (FIA)" moderata da Gregorio Consoli Chiomenti - Managing Partner con Mario Cortesi, DeA Capital Alternative Funds SGR - Managing Director, Guido Lombardo, Gardant Investor Sgr - Amministratore Delegato, Francesco Lombardo.Freshfields Bruckhaus Deringer - Partner, Paolo Pellegrini

Cerved Credit Management - Direttore Generale

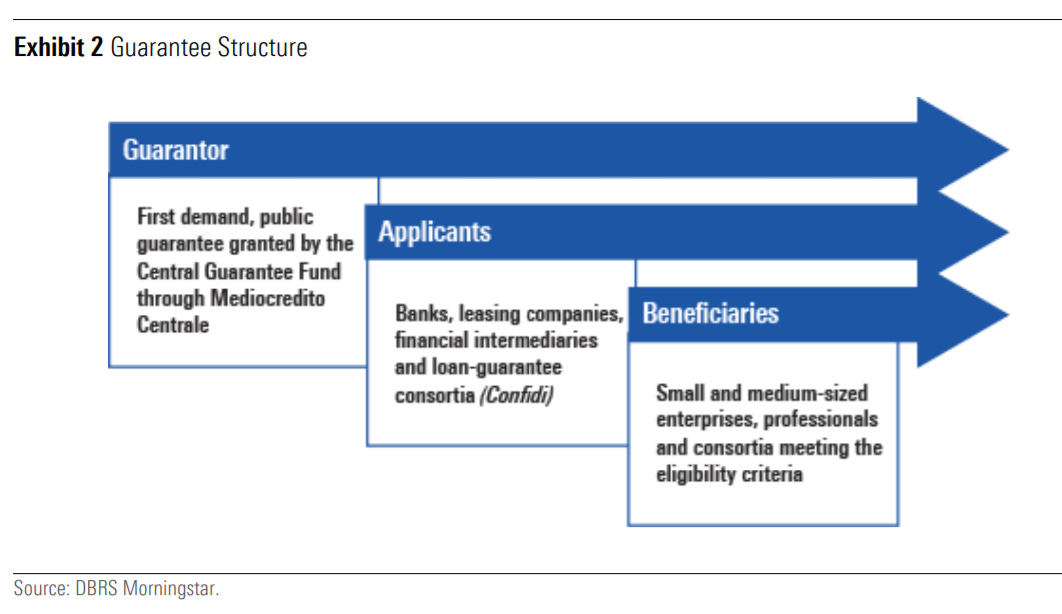

DBRS Morningstar published a commentary on Italian Central Guarantee Fund for SMEs deeming the Public Guarantee as a “Socially Relevant with Credit-Positive Implications”.

DBRS Morningstar believes that the CGF scheme provides positive social impact to the Italian SMEs as it acts as liquidity support to their business activity as well as to the banking sector as a mitigant to credit risk.

The guarantee is typically available to SMEs, professionals, and consortia regularly registered in Italy, with up to 249 employees and up to EUR 50 million in revenues, excluding companies operating in the financial sector. The Fund covers eligible medium- to long-term financial obligations (36 months or more) directly financing the business activity of the guaranteed entity, up to 80% of the financed amount, and up to EUR 2.5 million per borrower.

DBRS Morningstar believes that the positive social impact that the CGF scheme has on the Italian economy as a whole is twofold. On one hand, it provides relief to SMEs by easing access to liquidity that would otherwise be denied because of a number of constraints, such as lack of collateral, weak financial position, and general distressed economic environment. On the other hand, it acts as a credit risk-mitigating tool for the banking sector, absorbing losses that lenders may face upon the borrowers' default and thereby keeping a continuous flow of credit in the SME sector.

“We believe that the social impact of the guarantee remains in financing companies, which would otherwise not easily access the credit market or would do so at a higher cost,” said Ilaria Maschietto, Vice President of European Structured Credit at DBRS Morningstar. “The CGF scheme provides positive social impact to the Italian SMEs as it acts as liquidity support to their business activity as well as to the banking sector as a mitigant to credit risk,” Maschietto added.

In conclusion, DBRS consider CGF-guaranteed loans to be a positive credit factor in our analysis, providing a social benefit to the Italian SME sector. However, the guarantee might not necessarily be a key rating driver in most cases as other factors may prove to be more dominant and differ from transaction to transaction. As such, DBRS Morningstar will continue to analyse the merits of the guarantee in the context of each transaction and its structural features.