Key Fiscal Challenges for Italy

A recent report by Scope Ratings on fiscal policy and debt management

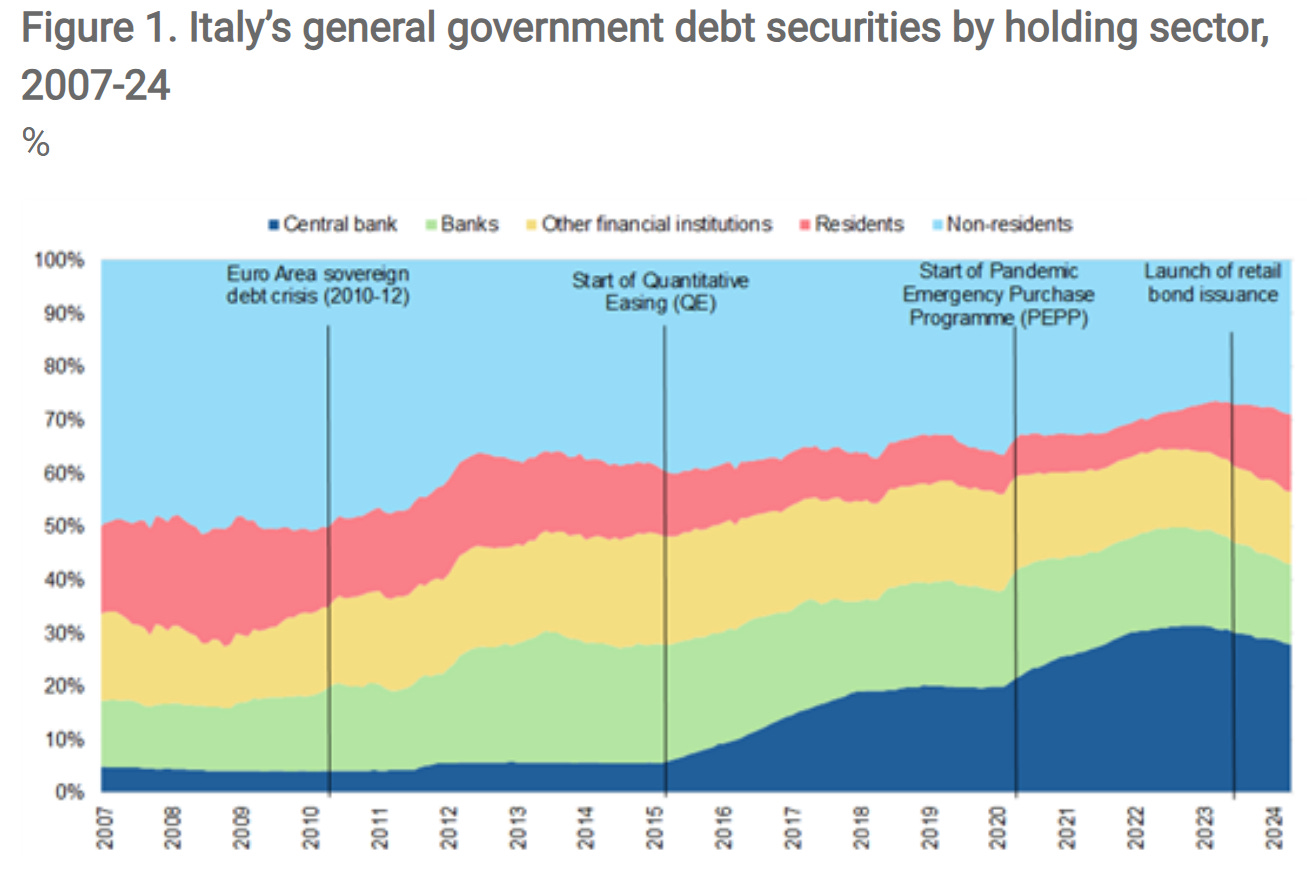

With an increasing share of Italian sovereign debt being held by foreign investors, the country faces heightened vulnerability to shifts in market sentiment. The rising reliance on these potentially less stable sources of demand underscores the necessity for Italy to implement a credible fiscal consolidation plan.

The European Commission's excessive deficit procedure, coupled with increased reliance on foreign investors, necessitates decisive fiscal measures. Without significant efforts to reduce persistent deficits, Italy’s general government deficit is projected to remain above 3% of GDP in the coming years. Consequently, the debt-to-GDP ratio is expected to rise from 137% in 2023 to 143% in 2029.

Fiscal Consolidation Requirements

Once the EU Council approves the procedure, Italy will need to undertake medium-term fiscal consolidation. This includes an annual fiscal adjustment of about 0.6% of GDP, achievable if the country maintains a minimum level of public investment aligned with the EU’s seven-year fiscal adjustment horizon.

Failure to meet these targets could render Italian debt securities ineligible for the European Central Bank's (ECB) Transmission Protection Instrument, a crucial mechanism designed to contain sharp rises in government bond yields. As the ECB reduces its holdings of Italian and other euro area sovereign debt, Italy’s susceptibility to foreign investors' risk appetite increases.

Domestic Retail Bonds as a Partial Solution

The introduction of BTP Valore bonds, aimed exclusively at retail investors, has helped increase the share of Italian government debt held domestically. Since the start of quantitative tightening (QT) in March 2023, domestic holdings of debt securities by Italian residents (excluding financial institutions) have surged by EUR 133 billion, reaching an all-time high of EUR 353 billion in April 2024. This has partially offset declines in ECB and financial institution holdings.

Despite this increase, domestic retail demand alone is unlikely to fully replace the gradual reduction in ECB holdings amid rising government debt. Current central bank holdings stand at around EUR 674 billion, necessitating continued demand from foreign investors.

Comparative Trends, Future Outlook and Key Measures

Italy's strategy mirrors trends in other high-debt euro area countries. Belgium, for instance, reintroduced medium and long-term State Notes in 2022, achieving record demand of EUR 21.9 billion in September 2023. Similarly, Croatia and Portugal have seen significant retail demand for their sovereign debt.

The latest issuance of BTP Valore bonds raised EUR 11.3 billion, exceeding expectations but falling short of previous issues. This slowdown in retail demand underscores the need for structural fiscal reforms and investments to stimulate economic growth while reducing public expenditure.

Conclusion

Italy’s fiscal future hinges on balancing the increasing share of foreign-held debt with robust domestic demand and comprehensive fiscal reforms. Ensuring stability in the face of changing market sentiments and ECB policies will require a concerted effort to implement sustainable fiscal policies and leverage domestic investment.

EU Banks: NPLs on the Rise

The European banking sector is bracing for a continued rise in non-performing loans (NPLs) despite expectations of modest economic recovery in the euro area. Scope Ratings' latest report reveals a concerning trend in the formation of NPLs across the region, driven by various economic and sector-specific factors.

Entering Italian NPE Market is a newsletter and a Linkedin Group focused on News, Updates and Insights on Italian Banks, Ditressed Credit Market, Fintech and Real Estate.

Relevant Links:

https://scoperatings.com/ratings-and-research/research/EN/177549

This newsletter is free please consider supporting it with a small donation

See my full professional profile (available for consulting projects)

My Podcast on Financial News and Education

My new Podcast on Italian Politics